RetirementCalculators.com.au

https://retirementcalculators.com.au/health-care-cards/ · Printed

Health Care Cards Explained: Which One Is Right for You?

There are three different health care cards Australians can hold, and almost everyone I speak with is unsure which one applies to them — or whether they qualify at all. The good news is that you almost certainly qualify for at least one of them once you understand which is which. This page is a friendly comparison of all three, with eligibility limits and what each card actually unlocks. Once you've read it, the eligibility calculator runs all three checks at once so you don't have to guess.

What's covered on this page

A side-by-side comparison of the three cards, the income limits that determine eligibility, what each card actually saves you on prescriptions and concessions, and the most common misconceptions that put people off applying.

Three Cards, Three Audiences

The three cards exist because they're aimed at three different groups. Once you know which group you're in, the right card is obvious.

PBS rates effective from 1 January 2026; concession card limits update with their respective indexation cycles.

Key Point 1: The Three Cards At a Glance

Each card is for a different group of people. Here's the quick comparison.

Pensioner Concession Card (PCC)

Issued automatically when you're approved for the Age Pension, Disability Support Pension or Carer Payment. No separate application.

Best benefits: the broadest of the three — PBS, bulk-billing, and most state and council concessions on rates, registration and utilities.

Read full PCC guide →Low Income Health Care Card (LIHCC)

For Australians of any age whose weekly income is under the threshold. Useful for people under Age Pension age or those who've never qualified for a pension.

Best benefits: PBS prescriptions at the concession rate, plus most state-government concessions (varies by state).

Read full LIHCC guide →Commonwealth Seniors Health Card (CSHC)

For people at Age Pension age who don't qualify for the pension itself, but earn under the income limit. Asset test doesn't apply.

Best benefits: PBS prescriptions at the concession rate and bulk-billed GP visits. Fewer state-level perks than the PCC.

Read full CSHC guide →Income limits side by side

| Card | Single income limit | Couple income limit | Asset test? |

|---|---|---|---|

| Pensioner Concession Card | Tied to Age Pension eligibility — see Age Pension | Yes (via pension test) | |

| Low Income Health Care Card | $811 / week | $1,385 / week | No |

| Commonwealth Seniors Health Card | $101,105 / year | $161,768 / year | No |

Note that the LIHCC limit is a weekly figure averaged over the previous 8 weeks; the CSHC limit is an annual figure based on adjusted taxable income from your most recent tax return. Different rules apply, even though both are income-only tests.

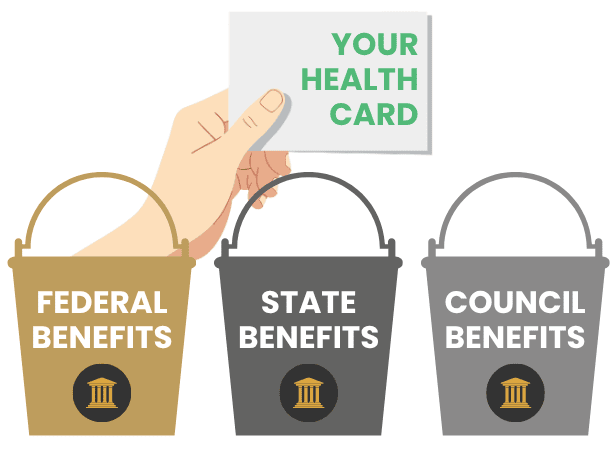

Key Point 2: What Each Card Actually Unlocks

The benefits split into three buckets — federal (which apply identically across all three cards or are similar), state-government (which vary considerably), and local council (which vary even more).

Three layers of savings. Federal is the same everywhere; state and council vary.

Federal benefits (PBS prescriptions and Medicare)

All three cards provide access to medicines on the Pharmaceutical Benefits Scheme at the concession price. The general PBS rate is currently $25.00 per script; with a card, you pay the concession rate of $7.70. Over a year of regular medication, the difference adds up substantially.

The PBS Safety Net kicks in once your annual prescription spending crosses a threshold — concession-card holders pay nothing further (current threshold: $277.20). All three cards also qualify you for bulk-billed GP visits at participating practices.

State-government concessions

Each state and territory runs its own concession schemes for cardholders. These typically include:

- Discounted vehicle registration and driver licence renewals

- Electricity, gas and water utility rebates

- Public transport concession fares (and free travel in some states)

- Council rate concessions (administered by local councils with state subsidy)

- Free or subsidised public dental schemes (waiting lists apply)

The PCC and LIHCC qualify for almost all state schemes. The CSHC qualifies for fewer — it's a federal card with limited state recognition. For the specific concessions in your state, see your state concessions guide.

An indicative savings example

💡 Rough order-of-magnitude

Most cardholders save several hundred to a few thousand dollars a year, depending on their state, their medication usage, and which concessions they actively claim. Heavy prescription users see the biggest PBS benefit; renters and homeowners see meaningful state-level savings on utilities and rates. The actual figure varies too much by state and personal circumstance to give a single number — but for most retirees, the combined annual saving comfortably exceeds the time it takes to apply.

For specific dollar values in your state, see your state concessions guide.

Key Point 3: Choosing the Right Card for Your Situation

The card you should apply for depends on your situation. Find the one that sounds most like you.

"I'm receiving the Age Pension already."

You already have the PCC

The Pensioner Concession Card was issued automatically when you were approved. If you can't find it, log in to myGov to access your digital card.

PCC details →"I'm at Age Pension age but earning too much for the pension."

Apply for the CSHC

The Commonwealth Seniors Health Card has no asset test, only an income test based on your tax return. Many self-funded retirees qualify.

CSHC details →"I'm under Age Pension age and on a low weekly income."

Apply for the LIHCC

The Low Income Health Care Card has no age limit and uses an 8-week income average. Useful for people not yet old enough for the pension or CSHC.

LIHCC details →"I'm not sure which I qualify for."

Run all three checks at once

The eligibility calculator screens you for all three cards simultaneously, returning eligibility for each.

Open the calculator →Common Misconceptions That Stop People Applying

From conversations with clients, the same handful of beliefs put off people who would actually qualify. Worth checking whether any of these are stopping you.

"I own my home, so I won't qualify."

Your home doesn't disqualify you.

The PCC follows pension eligibility (and the home is exempt from the pension assets test). The CSHC has no asset test at all — just an income test. The LIHCC is also income-only. Owning your home is irrelevant to all three.

"I have too much in super to get any help."

Super matters less than you think.

For the CSHC, the income test uses your adjusted taxable income — super in accumulation phase doesn't usually count, and the income from an account-based pension is calculated using deeming, which often gives a lower income figure than actual earnings. Many retirees with substantial super still qualify for the CSHC.

"I work part-time, so I'm not eligible."

Part-time work doesn't automatically disqualify you.

For the LIHCC, eligibility is based on an 8-week income average — short bursts of work don't necessarily push you over. For the PCC, the Work Bonus excludes a portion of work income from the pension test. Run your numbers before assuming.

"These cards are only for pensioners."

Two of the three are specifically for non-pensioners.

The CSHC exists for self-funded retirees who don't qualify for the pension. The LIHCC is for working-age people on low income. Only the PCC requires being on a Centrelink payment.

About the savings figures on this page

Concession amounts vary considerably by state, council, and individual circumstance — what your neighbour saves on rates may differ from what you save, even on the same card. Use this page for the framework and the federal-level figures (which are the same Australia-wide); for the specific dollar values that apply where you live, check your state's concessions guide. Concession schemes also change year-to-year as state budgets are updated.

If you're trying to work out whether applying is worthwhile, the safe answer is: almost always yes. The application is short, the assessment is straightforward, and the cost of not holding a card you'd qualify for is several hundred dollars a year minimum.

Frequently Asked Questions

Which health care card should I apply for?

It depends on your situation. If you receive the Age Pension, the Pensioner Concession Card comes automatically — no application needed. If you don't qualify for the pension but earn under the income limit, the Commonwealth Seniors Health Card is for self-funded retirees. If you're under Age Pension age and your weekly income is under the limit, the Low Income Health Care Card may apply. The eligibility calculator runs all three checks at once.

Can I hold more than one health care card?

Generally no — you'll qualify for the one that matches your situation. The PCC overrides the others if you receive the pension. The LIHCC and CSHC don't overlap because their eligibility criteria are mutually exclusive (one is for low-income working-age, the other for self-funded retirees over Age Pension age).

Do I need to be on the pension to get any health card?

No. The PCC requires being on a pension or eligible Centrelink payment, but the other two don't. The CSHC is specifically for self-funded retirees who don't qualify for the pension. The LIHCC is for anyone with weekly income under the threshold.

How often do I need to renew my health care card?

It varies by card. The PCC stays current as long as you receive the pension. The LIHCC is reissued every 12 months and you must reconfirm your income. The CSHC is reviewed annually based on your adjusted taxable income from your most recent tax return.

Do these cards cover dental and optical?

Concession cards don't directly cover dental or optical, but holding one usually qualifies you for state-government dental waiting lists and may give discounts on optical services. State and territory dental schemes vary widely — check your state's specific concessions page for what's available where you live.

Where to Next

Once you've worked out which card applies to your situation, the next step depends on the card. The PCC arrives automatically with the Age Pension — no separate application. The LIHCC and CSHC each have their own short application form lodged through myGov. Whichever path you're on, the eligibility calculator below tells you what you qualify for in five minutes, so you can stop guessing.

Find Out Which Cards You Qualify For

Five minutes with the eligibility calculator and you'll know exactly which of the three cards applies to your situation — no guesswork.

Accuracy Note: Whilst every effort has been made to provide current and accurate information, I am only one person and there's a very good chance that I'll miss something. If you spot a factual error, or if a calculator breaks or gives incorrect answers, I'd be really grateful if you could let me know via the Contact Us page so I can fix it ASAP.

It would speed up the correction process enormously if you could cite for me the title of the page where you find the error and describe what the error is. Thanks heaps for your support in keeping this valuable resource up to date for everyone's benefit.

Last reviewed: 9 May 2026 · All figures pulled live from the RC Data Engine. For previous indexation periods or other Centrelink rates, see the Centrelink Rates & Thresholds reference page.