RetirementCalculators.com.au

https://retirementcalculators.com.au/age-pension/ · Printed

The Age Pension: Your Complete Guide

The Age Pension is the main retirement income payment for older Australians, and most people approaching retirement want to know two things: am I eligible, and how much will I get? This hub is your starting point — a quick snapshot of the current rates, signposts to the right calculators for your situation, and links to deeper guides on each piece of the system. Pick where to dive in based on what you actually want to know.

What's covered in this section

Eligibility rules, the current rates and thresholds, plain-English guides to the income and assets tests, deeming rules, the Work Bonus and Rent Assistance — plus calculators that work out exactly what you'd receive. Everything you need to make confident decisions about the Age Pension.

Current Rates and Key Numbers

The headline figures, current at the latest indexation. These update automatically each March and September.

Effective from 1 July 2026. For previous indexation periods or other Centrelink rates, see the Centrelink Rates & Thresholds reference.

Key Point 1: Am I Eligible?

To qualify for the Age Pension, you need to satisfy three things — age, residency, and the means tests.

- Age — you must be at Age Pension age (currently 67) for everyone born after 1 January 1957.

- Residency — you must be an Australian resident with at least 10 years of residence, including 5 continuous years.

- Means tests — your income and your assets are both checked against thresholds. The pension you receive is the lower result from the two tests.

For the full eligibility rules including special situations, the Age Pension Eligibility guide walks through each requirement in detail.

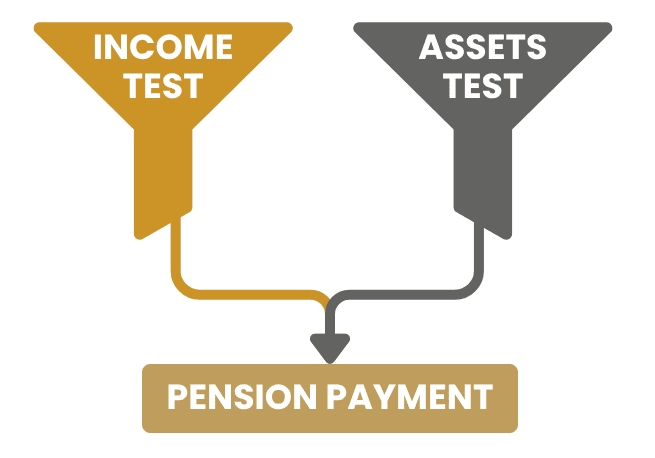

Key Point 2: How Much Will I Get?

Centrelink runs both means tests and pays whichever produces the lower result. The income test reduces your pension based on what you earn (including deemed earnings on financial assets). The assets test reduces your pension based on what you own — except for your principal home, which is fully exempt regardless of value.

Assets test thresholds at a glance

If your assets are below the lower threshold, you receive the full pension (subject to the income test). Above the upper threshold, the pension stops altogether. Between the two, you receive a part pension that reduces gradually.

| Situation | Full pension up to | Part pension cuts out at |

|---|---|---|

| Homeowner — single | $333,000 | $733,500 |

| Homeowner — couple combined | $499,000 | $1,102,500 |

| Non-homeowner — single | $600,000 | $1,000,500 |

| Non-homeowner — couple combined | $766,000 | $1,369,500 |

The fastest way to a real answer

Reading thresholds gets you so far. The How Much Age Pension Can I Get? calculator runs both tests with your actual numbers and shows your fortnightly result in about five minutes. Skip the maths.

Key Point 3: Planning Around the Age Pension

Most retirees aren't passive about the Age Pension — they're making decisions that interact with it. Find the situation that sounds most like yours.

"I want to keep working some hours."

Read: Work Bonus Explained

The Work Bonus excludes a portion of work income from the pension test, and any unused amount banks for later.

Open Work Bonus guide →"My partner is younger than me."

Read: Younger Partner Options

Your partner may have access to different payment types until they reach pension age themselves.

See younger partner options →"I'm renting in retirement."

Read: Rent Assistance

Pensioners who pay rent above a threshold may qualify for an additional supplement on top of the pension.

See Rent Assistance →"I have super or savings — how is it counted?"

Read: Deeming Rules

Centrelink applies an assumed earnings rate ("deeming") to financial assets rather than asking what they actually earned.

Understand deeming →All Age Pension Guides & Calculators

The full set of resources in this section.

Income Test Explained

What counts as income, what doesn't, and how the test reduces your pension.

Open guide →Assets Test Explained

What's assessable, what's exempt, and the thresholds that determine your pension.

Open guide →Deeming Rules

How Centrelink calculates earnings on your financial assets, with worked examples.

Open guide →Work Bonus

How working part-time interacts with your pension, including the unused-amount bank.

Open guide →Rent Assistance

Eligibility and rate of the additional supplement for pensioners who pay rent.

Open guide →How Much Can I Get?

The headline calculator — runs both means tests on your actual numbers in about five minutes.

Open calculator →Latest Indexation Impact

How the most recent rate changes affect single and couple pensioners — before vs after.

Open page →Younger Partner Options

Payments and considerations when one partner is below Age Pension age.

Open hub →All Rates & Thresholds

The complete current rate table, plus historical indexation periods.

Open reference →Mixed-Age Couple Calculator

A dedicated calculator for couples where one partner is under Age Pension age — currently being rebuilt. In the meantime, see the Mixed-Age Couple Guide.

Open guide instead →What This Page Won't Tell You

These situations need professional advice

Some retirement scenarios have substantial financial consequences from getting the structure wrong. If any of the following apply to you, please don't rely on online tools alone:

- Granny flat interests — moving in with family in exchange for transferring property or paying for a build is a complex area where Centrelink, ACAT and tax rules interact differently.

- Residential Aged Care planning — terminology and rules in this area have changed substantially in recent times and remain complex.

- Trusts, private companies and SMSF income — Centrelink's controller-attribution rules are technical and easy to get wrong.

If your situation involves any of these, please book a coaching call or talk to a financial planner who specialises in retirement and Centrelink.

Frequently Asked Questions

Who qualifies for the Age Pension in Australia?

To qualify, you must be at Age Pension age (currently 67 for everyone born after 1 January 1957), be an Australian resident with at least 10 years of residence including 5 continuous years, and pass both the income test and the assets test. The pension you receive is the lower result from the two tests.

Do I have to be retired to receive the Age Pension?

No. You can receive the Age Pension while still working — many recipients do. The Work Bonus excludes a portion of work income from the income test, and any unused bank rolls forward. Your eligibility depends on whether your overall income and assets keep you under the cut-off thresholds.

Does my home affect my Age Pension?

Your principal home is fully exempt from the assets test, regardless of its value. However, whether you own a home determines which assets-test threshold applies — homeowners have lower thresholds than non-homeowners. There's also a 2-hectare cap on adjacent land for rural properties.

What's the difference between a full pension and a part pension?

A full pension is the maximum rate, paid when your income and assets are both below the lower thresholds. As your income or assets rise above those thresholds, the pension reduces gradually — that's a part pension. The pension stops altogether at the upper cut-off points. Receiving even a small part pension still gives you the Pensioner Concession Card and its associated benefits.

When should I start the application process?

You can lodge a claim up to 13 weeks before reaching Age Pension age, which avoids any gap caused by processing time. There's no penalty for applying later — but you only get paid from the date you claim, so don't leave it indefinitely. See the Getting Started guide for the orientation, or the Step-by-Step Application Guide for the hands-on detail.

Where to Next

The Age Pension is a system of moving parts — eligibility, two means tests, deeming, supplements — but it's also a system most retirees come to terms with quickly once they engage with it. The fastest way to find your footing is to put your numbers into the How Much calculator, then dig into the specific guides for whatever you want to understand more deeply. There's no wrong starting point.

Ready to See What You'd Get?

Five minutes with the How Much calculator gives you a real answer based on your real numbers. Or book a one-on-one coaching call to walk through your situation in detail.

Accuracy Note: Whilst every effort has been made to provide current and accurate information, I am only one person and there's a very good chance that I'll miss something. If you spot a factual error, or if a calculator breaks or gives incorrect answers, I'd be really grateful if you could let me know via the Contact Us page so I can fix it ASAP.

It would speed up the correction process enormously if you could cite for me the title of the page where you find the error and describe what the error is. Thanks heaps for your support in keeping this valuable resource up to date for everyone's benefit.

Last reviewed: 9 May 2026 · All figures are pulled live from the RC Data Engine. For previous indexation periods, see the Centrelink Rates & Thresholds reference page.