RetirementCalculators.com.au

https://retirementcalculators.com.au/centrelink-made-simple/ · Printed

Centrelink Made Simple: Your Plain-English Starting Point

If you're approaching retirement and the word "Centrelink" makes your shoulders tense up, take a breath — you're in the right place. Most retirees I speak with feel the same way at first: the language is dense, the rules feel like a maze, and the application forms ask questions that don't seem to have plain-English answers. The good news is that once you understand how it's structured, the whole thing is much simpler than it looks. This page is your orientation map.

What you'll get from this page

A friendly walkthrough of the four main types of help available to retirees, a plain-English explanation of how Centrelink decides what you receive, and clear signposts to whichever calculator or guide is the right next step for your situation.

The headline numbers, right now

Three figures every retiree should know. These update automatically whenever the government indexes them.

Effective from 1 July 2026. For previous indexation periods, see the Centrelink Rates & Thresholds reference.

Key Point 1: The Four Buckets of Help Available to Retirees

Centrelink isn't one single payment — it's a collection of programs, and most retirees only need to think about four of them. Here they are in plain English.

The Age Pension

The main income payment for retirees. To qualify, you need to be at Age Pension age, an Australian resident, and pass both an income test and an assets test. You don't have to be "broke" to get it — many homeowner couples with substantial savings still receive a part pension.

Open the Age Pension hub →Health Care Cards

Three different cards, each unlocking cheaper prescriptions, bulk-billed doctors and various state and council concessions. The right one for you depends on whether you're on the pension, on a low income, or self-funded.

Open the Health Care Cards hub →Supplements & State Concessions

Add-ons that come with the pension or with a card — Pension Supplement, Energy Supplement, Rent Assistance — plus a long list of state-based concessions on rates, registration, utilities and travel.

See state concessions →Specialist Payments

Payments for specific situations — Carer Payment if you care for someone with a disability, or pre-Age-Pension-age payments for a younger partner of a pensioner.

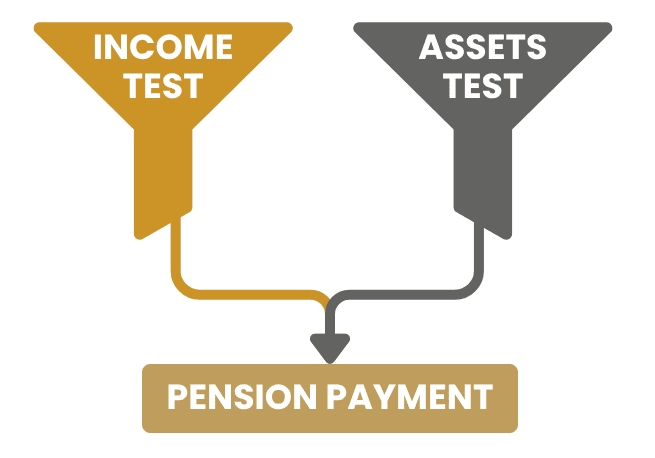

See younger partner options →Key Point 2: How Centrelink Works Out What You'll Get

Once you've put your hand up for the Age Pension, Centrelink runs two separate tests. You receive whichever one gives you the lower payment — that's deliberate, because they want to make sure neither test alone hands out too much.

The Income Test

Looks at money coming in — wages, foreign pensions, deemed earnings on your financial assets, rental income. Once your income exceeds an "income-free area", every dollar above it reduces your pension by 50 cents. The free areas are $226 per fortnight (single) and $396 per fortnight (couple combined).

The Assets Test

Looks at what you own — savings, super (once you reach Age Pension age), investments, vehicles, household contents. Your principal home is exempt regardless of value. Whether you own a home affects which threshold applies:

| Situation | Full pension up to | Part pension cuts out at |

|---|---|---|

| Homeowner — single | $333,000 | $733,500 |

| Homeowner — couple combined | $499,000 | $1,102,500 |

| Non-homeowner — single | $600,000 | $1,000,500 |

| Non-homeowner — couple combined | $766,000 | $1,369,500 |

Above the lower threshold the pension reduces gradually until the cut-out point, where it stops altogether.

A note on "deeming"

Centrelink doesn't ask what your savings or super actually earned this year. Instead it applies an assumed earnings rate ("deeming") to the balance — currently 1.25% on the first $66,800 for a single (or $110,600 for a couple combined), and 3.25% on anything above. This makes things simpler — but it can also mean Centrelink credits you with more (or less) earnings than you actually received.

Key Point 3: Where to Start, Depending on Your Situation

Different starting points need different first steps. Find the one that sounds most like you.

"I'm approaching pension age and want to know what I'd get."

Start with: How Much Age Pension Can I Get?

The calculator runs both means tests for you using your numbers, and shows the result. Five minutes start to finish.

Open the calculator →"I'm under pension age but my partner is on the Age Pension."

Start with: Younger Partner Options

You may have access to different payment types until you reach pension age yourself.

See younger partner options →"I don't qualify for the pension but I'd like help with health costs."

Start with: Health Care Cards Overview

Self-funded retirees can often qualify for the Commonwealth Seniors Health Card, which gives access to cheaper prescriptions and bulk-billed GP visits.

See the health card options →"I'd like one tool to check everything I might be entitled to."

Start with: Complete Entitlements Checker

Runs every relevant test in one go — Age Pension, all three health care cards, and supplementary payments.

Open the full checker →What This Page Won't Tell You

These situations need professional advice — not a website

Some retirement scenarios have substantial financial consequences from getting the structure wrong. If any of the following apply to you, please don't rely on online tools alone:

- Granny flat interests — moving in with family in exchange for transferring property or paying for a build is a complex area where Centrelink, ACAT and tax rules interact differently.

- Residential Aged Care planning — terminology and rules in this area have changed substantially in recent times and remain complex.

- Trusts, private companies and SMSF income — Centrelink's controller-attribution rules are technical and easy to get wrong.

If your situation involves any of these, please book a coaching call or talk to a financial planner who specialises in retirement and Centrelink.

Frequently Asked Questions

Do I have to apply for the Age Pension as soon as I turn the qualifying age?

No. There's no automatic enrolment and no penalty for applying later. You can lodge your claim up to 13 weeks before you reach Age Pension age, or any time after. The catch is that you only get paid from the date you claim — Centrelink generally won't backdate, so don't leave it indefinitely.

Can I still get Centrelink help if I'm working part-time?

Yes. The Work Bonus excludes a portion of work income from the Age Pension income test. Many retirees draw a part pension while still doing some paid work. Whether you qualify in your specific situation depends on your overall income and assets — the How Much calculator works this out for you.

Does my superannuation count toward Centrelink tests?

Before you reach Age Pension age, your superannuation is generally not assessed as an asset by Centrelink. Once you reach Age Pension age, your super becomes a financial asset and is included in both the income test (via deeming) and the assets test.

Does my home count as an asset?

Your principal home is fully exempt from the assets test, no matter what it's worth. However, whether you own a home determines which assets-test threshold applies to the rest of your assets — homeowners have lower thresholds than non-homeowners. There's also a 2-hectare land cap to be aware of for rural properties.

What's the difference between the Pensioner Concession Card and the Commonwealth Seniors Health Card?

The Pensioner Concession Card (PCC) is automatic with the Age Pension and gives the broadest concessions, including state-government benefits like cheaper rego and utility rebates. The Commonwealth Seniors Health Card (CSHC) is for self-funded retirees who don't qualify for the pension but earn under the income limit (currently $101,105 single, $161,768 couple). It mainly gives access to PBS prescriptions at the concession rate and bulk-billed GP visits — fewer state-level perks than the PCC.

Where to Next

Centrelink for retirees boils down to four buckets of help, two means tests, and a starting point that depends on your situation. The figures above will change every March and September as the government indexes them — but the structure stays the same year after year, so the time you spend understanding it now will serve you for the rest of your retirement. Pick the calculator or guide that matches your situation, and work through it slowly. There's no rush, and there's no wrong starting point.

Ready to Check What You're Entitled To?

Take five minutes with the How Much calculator, or book a one-on-one coaching call to walk through your situation in detail.

Accuracy Note: Whilst every effort has been made to provide current and accurate information, I am only one person and there's a very good chance that I'll miss something. If you spot a factual error, or if a calculator breaks or gives incorrect answers, I'd be really grateful if you could let me know via the Contact Us page so I can fix it ASAP.

It would speed up the correction process enormously if you could cite for me the title of the page where you find the error and describe what the error is. Thanks heaps for your support in keeping this valuable resource up to date for everyone's benefit.

Last reviewed: 9 May 2026 · All figures shown are pulled live from the RC Data Engine. For previous indexation periods, see the Centrelink Rates & Thresholds reference page.